(Kent State University, 2013)

With the recession still on America's heels the financial chaos in higher education is still effecting future and current students (Romano). The cost of an higher education has become reasonably unattainable for many students. Tuition rates have outpaced national inflation and the productivity of education has failed to improve at an identical rate. The income of many families can not keep up to pace with the skyscraper cost of a post-secondary education. Thus there seems to be a correlation between first generation college students coming mostly from low-income families. Their parents were not able to afford a college education therefore making their children's possible college experience just a fanciful dream.

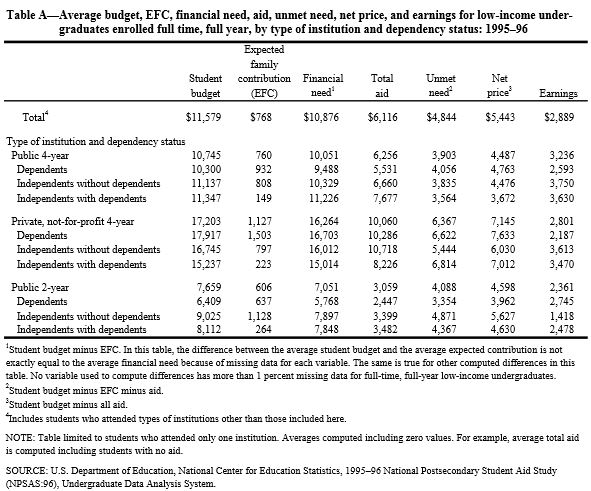

The Financial NeedSusan P. Choy published a report entitled "Low-Income Students: Who They Are and How They Pay for Their Education," that studied the substantial financial need for low-income families. Financial need is the difference between the price of attending a post-secondary institution and what the student is expected to pay based on the family’s financial circumstances. Table 2 shows the average budget, EFC, financial need, aid, unmet need, net price, and earnings for low-income undergraduates enrolled full time at different types of institutes as studied by Choy.

The expected family contribution (EFC) is determined by a formula that takes into account family income and assets, family size, and the number of other college students in the family. The formula for EFC has changed many times over the years as policy makers strive to make it fair. There are issues such as at what age should a student's income not be considered with their parents. The student aid is limited therefore it's distribution must be handled carefully and appropriately. |

Table 2. shows the average budget, EFC, financial need, aid, unmet need, net price, and earnings for low-income undergraduates enrolled full time at different types of institutes. (Choy) Click for larger image.

|

The financial need is accommodated for through different types of aid. The aid can be federal, state, or even institutional. Most low-income students receive grant such as the Federal Pell Grant. Another important source is loans. Many loans available for students do not accrue interest until six months after they graduate perpetually giving them "time" to acquire a job and earn a stable income.